Key takeaways

- The neobank market is expected to grow from $230B in 2025 to $ 4.39 trillion by 2034 at a 26.7% CAGR.

- Neobanks are relying on fintech vendor ecosystems to launch banking services faster.

- Vendor partnerships help neobanks reduce infrastructure costs while accelerating product launches.

- Digital banking ecosystems are replacing traditional banking infrastructure with scalable fintech integrations.

Launching a neobank isn’t about building every system from scratch. Instead, it’s about assembling a network of specialized vendors for infrastructure, compliance, payments, and customer experience

Traditional banks used to build almost everything in-house, but not anymore. As fintech startups building neobanks play by different rules. They plug into an ecosystem of modular vendors to roll out digital banking services faster and with less hassle.

And, this approach is not just efficient, it’s necessary. Digital banking is not slowing down. By 2034, the global neobanking market is expected to expand from $230.55 billion in 2025 to around $4.39 trillion, driven by rising digital adoption and demand for mobile banking.

With this kind of momentum, fintechs can’t afford to get sloppy. Choosing the right partners is crucial if they want to build digital banking platforms that feel secure, meet regulations, and scale as the market expands.

That’s where the Goodfirms neobank development vendor recipe and tech stack guide comes in. We have laid out the whole vendor landscape, helping fintech founders find vetted partners across infrastructure, compliance, development, and growth. In short, it’s a roadmap to help fintech startups, founders, and investors launch and scale their neobank without getting lost in the weeds.

Caveat: Understanding the Neobank Vendor ecosystem is the first step toward building a successful digital bank.

What Is a Neobank Vendor Ecosystem?

A neobank vendor ecosystem comprises a network of third-party technology providers, banking partners, and a sector of fintech specialists that offer various financial services to power a digital bank.

Instead of developing all systems internally, neobanks integrate services from multiple vendors, including:

- Banking-as-a-Service providers

- Payment processors

- Compliance and identity verification vendors

- Fraud detection and cybersecurity platforms

- App development and fintech UX design companies

This modular architecture is perfect for building neobanks, allowing fintech startups to launch faster, innovate continuously, and drive growth globally without building traditional banking infrastructure.

Why Neobanks Rely on Vendor Ecosystems?

Traditional banks spend years, including high budgets, on building internal infrastructure. Neobanks take a different approach by integrating specialized fintech vendors through APIs. Today, neobanks rely on vendor ecosystems due to cost efficiency.

Digital banks can operate with 60–70% lower acquisition and infrastructure costs compared with traditional banks, thanks to cloud infrastructure and fintech integrations.

This Vendor Ecosystem Model Provides Several Advantages:

- Faster Time-to-market

Startups can skip the time-consuming work of finding the best neobank vendors through various categories. By leveraging the pre-built banking infrastructure, fintechs can easily launch financial products in months rather than years.

- Reduced Development Costs

Fintech may require a high budget to building banking infrastructure from scratch. The designed vendor ecosystems make it effortless for fintech companies to reduce neobank app development costs.

- Access to Specialized Expertise

Fintechs can get access to different vendors focused on specific functions, such as BIN sponsors, compliance firms, development companies, etc, ensuring higher-quality services.

Because of these benefits, most modern neobanks operate through partner-driven technology stacks rather than fully proprietary systems.

The Vendor Ecosystem Powering Modern Neobanks

From licensing and regulatory compliance to developing, launching, and scaling a neobank, it requires expertise and trusted partnerships across several specialized vendor categories. As each of them plays a crucial role in ensuring the platform is built perfectly, that operates securely, efficiently, and in compliance with financial regulations.

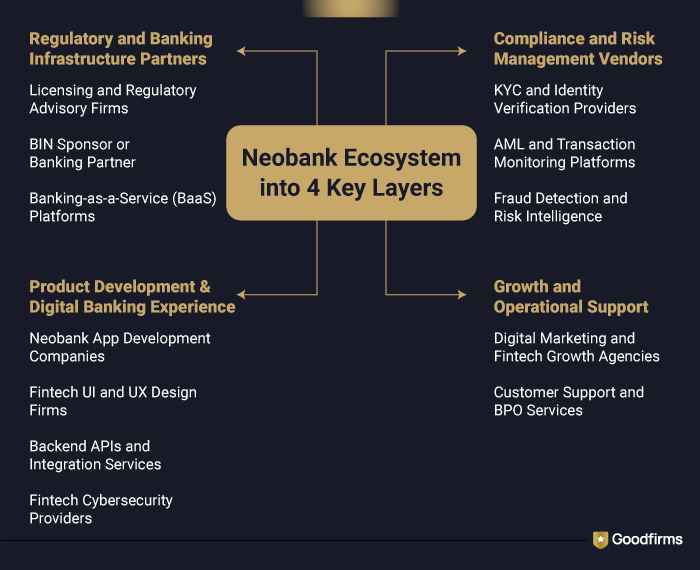

The Goodfirms Neobank Development Model breaks the neobank ecosystem into four essential layers—an approach that can make the difference between a successful launch and a project left awash.

Top Neobank Technology Providers & Platforms

A neobank or digital banking platform needs a complete fintech ecosystem, and leading software providers that enable faster go-to-market, seamless integrations, and scalable infrastructure.

1. Regulatory and Banking Infrastructure Partners

Every neobank must establish a regulatory and financial infrastructure foundation before launching services. The first layer covers the licensing models, sponsor banks, and BaaS choices.

- Licensing and Regulatory Advisory Firms

The financial and compliance regulations will surely be different across countries; Regulatory compliance consulting firms help fintech startups ensure the right regulatory compliance, making it a critical step during early planning.

Typical capabilities include:

- Understand licensing requirements

- Structure banking partnerships

- Comply with financial regulations

These experts ensure that the neobank operates legally within its target market.

- BIN Sponsor or Banking Partner

Most top fintech companies lack in holding full banking licenses. To get it, they partner with third-party BIN Sponsorship Partners & Providersthat offer them access to regulated financial infrastructure.

Typical capabilities include:

- Deposit accounts

- Payment network access

- Regulatory coverage

Without this BIN sponsor partnership, fintech startups cannot legally provide core banking services.

- Banking-as-a-Service (BaaS) Platforms

Banking-as-a-Service (Baas) providers deliver banking capabilities through APIs. This model helps neobanks offer banking services without becoming banks themselves.

Typical capabilities include:

- Account creation

- Payment processing

- Card issuing

- Transaction management

Banking as a service (BaaS) platforms have become the operational backbone of neobanks to ease the launch of digital financial products.

2. Compliance and Risk Management Vendors

Once the banking infrastructure is established, the next priority is maintaining regulatory compliance to meet strict standards to protect consumer assets and the platform from financial crime.

- KYC and Identity Verification Providers

KYC verification software for neobanks is required for verifying customer identities in real time during onboarding. These systems are best-fit to prevent fraud and monitor risks while meeting regulatory requirements.

Typical capabilities include:

- Identity document verification

- Biometric authentication

- Risk scoring

Automated identity verification also enables faster and more seamless onboarding experiences.

- AML Compliance and Transaction Monitoring Platforms

Anti-money laundering solutions specialize in monitoring financial transactions to detect suspicious activity. The AML software designed for fintech continuously analyzes transactions, behaviour, and anomalies, identifying patterns to mitigate financial crime risks.

Typical capabilities include:

- Track unusual transactions

- Generate compliance reports

- Prevent financial crime

Advanced monitoring platforms often use machine learning to identify risk patterns and provide monitoring solutions.

- Fraud Detection and Risk Intelligence

Fraud detection software platforms help digital banking platforms in monitoring user behavior and transaction patterns to block suspicious activities and potential fraud attempts.

Typical capabilities include:

- Account takeover

- Payment fraud

- Identity theft

Strong fraud detection systems provide capabilities that are essential for maintaining customer trust and regulatory compliance.

3. Product Development and Digital Banking Experience

As the compliance and infrastructure layers are done, the fintech teams move their focus to the next step, which is product development and designing the digital banking experience.

- Neobank App Development Companies

Neobank development companies are experts in building fintech apps, digital wallets, and payment applications, integrating the latest advancements in modern banking technologies.

Typical capabilities include:

- iOS and Android banking apps

- Digital payment features

- Integration with banking APIs

- Scalable backend infrastructure

Neobank app development partners play a crucial role in turning banking capabilities into a functional digital product.

- Fintech UI and UX Design Firms

User experience is a major competitive advantage for neobanks. Specialized fintech web design agencies create intuitive interfaces to reduce cognitive load, enhance engagement, and simplify financial management for users.

Typical capabilities include:

- Customer journey design

- Onboarding flows

- Financial dashboards

- Mobile banking interfaces

A well-designed experience helps digital banks foster user trust and improve customer retention.

- Backend APIs and Integration Services

Dedicated API developers are the architects of the modern financial ecosystem, helping to manage the complex web of integrations and functionalities to build an established banking infrastructure.

Typical capabilities include:

- Core banking systems

- Payment processors

- Compliance tools

- Card networks

Reliable integrations ensure smooth transaction processing and platform scalability.

- Fintech Cybersecurity Providers

Fintech cybersecurity companies protect neobanking platforms from data breaches, sophisticated attacks, and infrastructure vulnerabilities by implementing multi-factor authentication and AI-driven fraud detection.

Typical capabilities include:

- Security audits

- Penetration testing

- Threat monitoring

Given the sensitive nature of financial data, a robust cybersecurity infrastructure is vital for digital banks, from an IT concern to a strategic security protocol.

4. Growth and Operational Support

After launching, neobanks, the fintech companies require additional vendors to acquire customers and deliver operational support.

- Digital Marketing and Fintech Growth Agencies

Customer acquisition is a crucial thing for neobank growth to keep moving ahead in the market, strengthening loyalty, and enhancing engagement. Fintech digital marketing agencies are assisting organizations in leveraging targeted strategies to acquire customers at a lower cost than traditional methods.

Typical capabilities include:

- Digital advertising

- Fintech brand positioning

- User acquisition campaigns

Strategic marketing helps digital banks scale their user base quickly by optimizing user experience, boosting conversion rates, and fostering trust through personalized content.

- Customer Support and BPO Services

Fintech customer support services handle back-office operations and risk management processes for digital banking platforms, helping them maintain superior customer service and sustain growth.

Typical capabilities include:

- Onboarding assistance

- Payment dispute resolution

- Account management support

These partners assist neobanks in maintaining service quality and gaining a competitive edge with scalable support.

Example Neobank Tech Stack

A typical neobank integrates vendors across multiple layers:

|

Layer |

Example Vendor Category |

|---|---|

|

Licensed Banking Partner |

BIN Sponsors |

|

Banking Infrastructure |

Bank-as-a-Service (BaaS) Platform |

|

Compliance |

KYC / AML Vendors |

|

Payments |

Card & Payment Processors |

|

Fraud Prevention, Payment Risk |

Fraud & Risk Management Platforms |

|

Product Development |

Fintech App Development |

|

Security |

Fintech Cybersecurity Providers |

This ecosystem architecture allows fintech companies to build flexible and scalable digital banking platforms.

How Vendor Ecosystems Drive Neobank Growth?

Vendor ecosystems give fintech startups a real edge. They help neobanks get up and running faster, stay compliant, and ensure security isn’t just an afterthought.

Key advantages include:

- Faster product development cycles

- Reduced infrastructure costs

- Easier regulatory compliance

- Continuous product innovation

Platforms like Goodfirms are making it effortless for fintech founders to find trusted partners across the entire development lifecycle by spotlighting the top vendors in categories for ecosystem frameworks.

Bottom Line:

Launching a neobank takes much more than just developing a mobile banking application. The best digital banks lean on a handpicked ecosystem of vendors. These partners cover everything from regulatory expertise, robust neobanking infrastructure, compliance tools, payments, and customer experience. When founders really understand how these vendor layers fit together, they can map out their tech stacks with confidence and hit the market sooner.

Resources like the Goodfirms Neobank Development Vendors Recipe take a lot of the guesswork out of the process. The breakdown of the fintech ecosystem and the provision of the perfect layers with clear categories, connecting new banks with technology partners they can actually rely on.