Key takeaways

- White-label neobank is the fastest way to launch a digital bank in 2026, reducing development time to as little as 6–12 weeks.

- Startups can build a neobank without a license by leveraging Banking-as-a-Service (BaaS) partnerships.

- The cost to build a neobank in 2026 ranges from $25K to $100K+, depending on customization and integrations.

- Choosing between white label vs custom neobank vs BaaS depends on your speed, budget, and control requirements.

- A strong neobank architecture (APIs, KYC, payments, cloud) is critical for scalability.

- Compliance (KYC, AML, GDPR) should be planned early to avoid delays and penalties.

- Industries like SMEs, crypto, and e-commerce are rapidly adopting embedded finance infrastructure.

The Banking Revolution is Here

Five years ago, launching a digital bank meant years of development (18–24 months), millions of dollars ($500K–$2M), and navigating impossibly complex regulations with specialists on every team. Today? You can launch a fully-branded digital bank in 3 months or less with a budget of $25K–$100K.

This is the white-label neobank revolution of 2026. The infrastructure that used to be locked behind bank vaults is now accessible to startups, SMEs, and established companies looking to add financial services.

But here's the honest truth: not all white-label neobanks are equal, hidden costs can triple your budget, and choosing wrong can delay your launch by months or completely kill your project. Compliance mistakes can result in regulatory shutdowns. The "cheapest" solution often becomes the most expensive over time.

This guide gives you the real breakdown on costs, timelines, compliance, and vendor selection based on actual launches in 2026.

Explore top-rated neobank development companies to compare platforms, pricing, and verified client reviews before choosing your white-label neobank partner

What Is a White-Label Neobank? Understanding the Core Concept

A white-label neobank is a ready-made digital banking platform you customize and launch under your own brand. Instead of building from scratch, you leverage existing infrastructure.

What You Don't Have to Build:

- Core banking systems (accounts, transactions, ledgers) - Takes 6-9 months to build custom

- Payment infrastructure (cards, transfers, settlements) - Months to integrate with networks

- Compliance frameworks (KYC, AML, monitoring) - Banks spend millions annually

- Cloud infrastructure and security - Enterprise systems cost $50K+/month

- Mobile and web applications - Dev teams cost $200K+/year

What You Get Instead.

- A functioning digital bank ready to launch

- Your own branding and custom UI/UX

- API integrations that work out of the box

- Built-in compliance, regularly updated

- 24/7 infrastructure support and monitoring

- Regular security updates

Think of it like: You get the foundation, structure, plumbing, and electrical systems. You add paint, furniture, and décor to make it yours.

It is: Fast to launch (weeks, not years), modern and scalable, 70% cheaper than custom builds per Deloitte, proven globally.

It isn't: A fully independent bank, a "set and forget" solution, zero effort, or a complete white-glove service. To evaluate real platforms, browse leading white-label banking service providers offering ready-to-launch infrastructure.

White-Label vs. BaaS vs. Custom Build: Which Model Should You Choose?

Understanding the three approaches is critical because each has trade-offs: Building a neobank isn't a one-size-fits-all decision. Your choice depends on three factors: how fast you need to launch, how much you can budget, and how much control you need over your platform. Let's break down each approach.

White-Label: You get a pre-built platform, customize the branding and features, launch fast and affordably, but have less customization flexibility. This is like buying a franchise, branded and ready, but you follow their playbook.

BaaS: You get access to banking infrastructure and licensing, can build custom features on top, have more control and flexibility, but higher costs and a longer timeline.

Custom: You build everything from scratch, maximum control, maximum cost, maximum time investment. Only makes sense if you have $500K+ and can wait 18+ months.

|

Model |

Cost |

Time |

Control |

Best For |

|

White-Label Neobank |

$25K–$100K |

1–3 months |

Medium |

Startups wanting speed |

|

BaaS |

$50K–$200K |

3–6 months |

High |

Scaleups needing flexibility |

|

Custom Build |

$250K+ |

9–18 months |

Full |

Banks and enterprises |

The smart strategy most startups use: Start with white-label to validate your business model and get traction. Once you have 100K+ users and proven unit economics, migrate to BaaS for more control and customization. Build custom only if you've achieved product-market fit at scale. If you're comparing capabilities, reviewing the best banking software can help you understand real-world differences.

Essential Features Every Neobank Must Have

According to Juniper Research, global digital banking users will exceed 4.2 billion by 2026. This means your competitors already have these features; you need them too.

Non-Negotiable Features:

- Digital Onboarding with KYC software - Verify customers instantly, stay compliant

- Multi-Currency Accounts - Serve global customers

- Virtual & Physical Cards - Instant or physical issuance

- Real-Time Payments - Instant transfers between accounts

- Fraud Detection - AI-powered systems catching suspicious activity

- Analytics Dashboards - Real-time operational insights

- AI-Powered Personalization - Recommend products, predict customer needs, build loyalty

Personalization isn't optional anymore; it's your competitive advantage. Customers expect their neobank to understand their needs and serve them intelligently. Banks that deliver personalized experiences drive higher engagement, lower churn, and better unit economics.

Real Costs to Build a White-Label Neobank in 2026: The Complete Breakdown

Launching a white-label neobank is affordable compared to building custom, but most founders underestimate the total costs. They focus only on platform licensing and forget about the hidden expenses that add up fast. Let's be brutally honest about every cost category.

Initial Cost Breakdown: What You'll Actually Spend

|

Component |

Cost Range |

|

Platform License |

$20K–$50K |

|

Customization & Design |

$10K–$30K |

|

Compliance Setup |

$5K–$20K |

|

Third-Party Integrations |

$5K–$15K |

|

Monthly Maintenance |

$1K–$5K/month |

Total Initial: $25K–$100K

Platform License ($20K–$50K): Your biggest upfront expense. Basic platforms cost $20K. Feature-rich platforms with lending tools and advanced analytics cost $50K+.

Customization ($10K–$30K): Making the platform yours. Basic customization: $5K–$10K. Full customization with unique workflows: $20K–$30K.

Compliance Setup ($5K–$20K): Non-optional. Includes legal review, KYC/AML configuration, and documentation.

Integrations ($5K–$15K): Connecting payment gateways, analytics, and other services.

The Hidden Costs Nobody Talks About (And Why They Matter)

This is where launches get expensive. These recurring costs add up fast and catch many founders off guard.

- Revenue Sharing: BaaS partners take 20–40% of transaction fees, and the ongoing cost

- Regulatory Updates: Budget $2K–$5K annually for compliance changes

- Infrastructure Scaling: Server costs increase exponentially as users grow

- Customer Support: Budget $5K–$20K/month for 24/7 operations once live

- Marketing & Acquisition: Expect $50K–$200K to acquire your first customers

- Ongoing Compliance: Budget $500–$2K/month for legal and monitoring

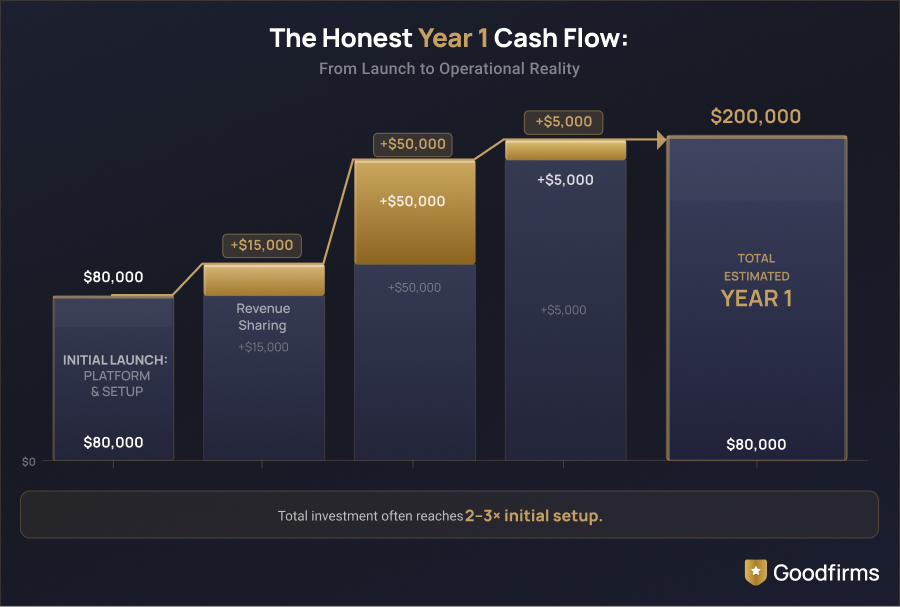

Real-World Example: The Freelancer Neobank Budget

Let's walk through a realistic budget for a neobank targeting freelancers with features for invoicing, payments, and tax savings.

- Platform license: $35K

- Customization: $20K (custom dashboard, integration with accounting tools)

- Compliance: $15K (legal review, KYC/AML setup, documentation)

- Integrations: $10K (payment gateways, Stripe, Wise, analytics tools)

- Launch Cost: $80K

- Year 1 total (including support, maintenance, marketing): ~$200K

This is what honest numbers look like. Not cheap, but dramatically cheaper than the $500K–$2M custom build approach.

According to Deloitte, fintech infrastructure costs are reduced by up to 70% using BaaS and white-label solutions compared to custom builds. When you do the math, a custom build costs $500K–$2M over 18 months. A white-label costs $25K–$100K and launches in 3 months. That's not just cost savings, that's market advantage.

Launch Timeline: How to Get to Market in 6-12 Weeks (Not 18 Months)

Speed is the biggest advantage of white-label neobanks. But speed requires proper planning and vendor alignment. Let's break down a realistic timeline.

|

Phase |

Duration |

Key Activities |

Deliverables |

|

Phase 1: Vendor Selection & Negotiation |

Weeks 1-3 |

Research platforms, demo testing, contract negotiation, and legal review |

Signed vendor agreement, platform access |

|

Phase 2: Implementation & Integration |

Weeks 4-9 |

API integration, database setup, payment gateway connection, UI customization |

Functioning backend, branded frontend |

|

Phase 3: Compliance Configuration |

Weeks 4-10 (parallel) |

KYC/AML rule setup, regulatory documentation, compliance testing |

Compliant platform, audit-ready |

|

Phase 4: Testing, QA & Refinement |

Weeks 9-12 |

Security testing, user testing, bug fixes, performance optimization |

Production-ready platform |

|

TOTAL time to market |

6–12 weeks |

- |

Live neobank accepting customers. |

Why This Timeline Matters for Your Business

10x Faster Than Custom Build

Custom builds take 9–18 months. White-label takes 1-3 months. That's a massive advantage:

- Test your idea with real users before full investment

- Get early market feedback and iterate

- Pivot based on customer response

- Build revenue before competitors launch

- Attract investors with real traction

To see how these costs scale across different product tiers, check our Neobank App Development Cost Guide.

Compliance: KYC, AML & Regulatory Requirements

Ignore compliance and face legal shutdowns, government fines ($10K–$1M+), and platform closure. Don't risk it.

What You Legally Need:

- KYC (Know Your Customer) - Verify every customer's identity

- AML (Anti-Money Laundering) - Monitor and report suspicious transactions

- Data Protection - GDPR, CCPA, and regional privacy laws compliance

- Regional Licensing - Different rules in the EU, US, Asia, etc.

Most startups build neobanks without a banking license by partnering with a licensed bank through BaaS providers. Your BaaS partner handles the license and regulatory cover. You handle the customer experience. This is legal, common, and the fastest path forward.

Industries Adopting White-Label Neobanks in 2026

White-label neobanks aren't just for fintech startups anymore. Entrepreneurs in diverse industries are launching banking platforms to serve their specific customer bases.

- SMEs - Embedded finance for business banking

- Crypto Platforms - Fiat on/off ramps for cryptocurrency exchanges

- E-Commerce Brands - Embedded payment solutions for online stores

- Gig Economy Platforms - Instant payouts for drivers, workers, freelancers

- Travel & Remittance Apps - Multi-currency international transfers

According to Statista, the embedded finance market is projected to exceed $7 trillion by 2030. Banking is moving inside apps. Your app might be next.

Choosing the Right White-Label Neobank Provider: How to Avoid Costly Mistakes

Your choice of neobank development company will determine whether you launch on time or miss deadlines, whether costs stay controlled or balloon, and whether your platform is reliable or constantly down.

Red Flags to Avoid:

- "Instant launch in days" (6–12 weeks is realistic)

- Vague compliance support

- Limited API flexibility

- Poor UI/UX in demos

- Hidden pricing models

What to Actually Evaluate:

- Verified Client Reviews - Check Goodfirms for real feedback

- Fintech Expertise - Do they understand banking and compliance?

- Tech Stack & Scalability - Can it handle 1M+ users?

- Compliance Track Record - Have they launched neobanks that still operate?

- Global Support - 24/7 support in your timezone?

- Case Studies - Ask for references and talk to actual customers

A few reference points for comparison:

Treezor and Railsbank (now Railsr) are established BaaS providers in Europe with full licensing support.

Synapse and Unit are US-focused BaaS platforms commonly used by early-stage fintechs.

For white-label front-end layers, providers like Mambu (core banking) and Thought Machine are used by larger scaleups, while lighter platforms like Alviere serve mid-market budgets.

These aren't endorsements, they're a starting point for your own diligence. Always request live references and ask about their compliance track record in your target market.

2026 Trends Shaping Neobank Development

If you're launching a neobank, you're not just building for today; you're building for 2026's competitive landscape. Here are the trends that will determine winners and losers.

- AI-Powered Banking - Personalized insights, smart fraud detection, helpful chatbots

- Crypto + Fiat Integration - Buy crypto directly from neobanks

- Embedded Finance Everywhere - Banking inside ride-sharing, e-commerce, marketplaces

- Hyper-Personalization - Every customer sees a customized interface

- Open Banking APIs - Third-party apps tap into your neobank

The neobank that wins in 2026 will be the one that understands its customers best. The banks that deliver personalized experiences, support crypto and fiat seamlessly, and embed themselves into users' daily apps will capture market share.

Conclusion: Is White-Label Neobank Right for You?

White-label neobanks aren't a future trend; they're happening right now in 2026. The barriers to entry have completely collapsed. Any startup with vision and execution can now launch a branded digital bank in weeks, not years.

But this opportunity comes with responsibility. Launching successfully comes down to four decisions: (1) choosing the right infrastructure model (white-label, BaaS, or custom), (2) selecting a vendor with a verifiable compliance track record, (3) budgeting honestly for hidden costs and Year 1 operations, and (4) timing your launch to get market feedback before over-investing in customization.

Frequently Asked Questions

1. Can I really build a neobank without a banking license?

Absolutely. By using Banking-as-a-Service (BaaS) for startups, you operate under the license of a "Sponsor Bank." They handle the balance sheet and regulatory oversight, while you focus on the customer journey.

2. Is white-label neobank development profitable in 2026?

Yes, but only if you move beyond simple transaction fees. Profitable neobanks today use neobank monetization strategies like interchange fees, premium subscription tiers, and SME lending.

3. How does AI improve my neobank's performance?

AI-powered neobanks use predictive analytics to offer users automated savings plans, personalized investment advice, and real-time fraud detection. This not only lowers operational costs but also significantly increases user "stickiness".

.jpg)