Taking any business off the ground requires an excellent idea, great dedication, and, of course, starting capital. Entrepreneurs can raise their finances from personal savings, early-stage investors, borrow through banks or bonds or sell their stock. However, by bootstrapping the startup, you can build a self-sustaining, financially-fit business.

Nowadays, businesses often begin without having established customers. All they have is an idea for a service or a prototype of a product. Starting without the support of venture capital or angel investment also has its own share of challenges and risks. Still, letting people know about your brand with a good website or an app can help you build a loyal customer base and give your startup the necessary push. Ultimately, with a clear vision, professionalism, and resilience, you can survive against all the odds, start earning profits and achieve your goals.

Goodfirms surveyed 260 early-stage business owners and experts worldwide to know the challenges a bootstrapping startup faces and the tips to overcome them.

What Is Bootstrapping In Business?

Bootstrapping is a business practice where a founder works on an idea and starts with limited resources and personal finances. In such cases, they don't usually take the help of outside capital and continue to scale the business by reinvesting the net profit.

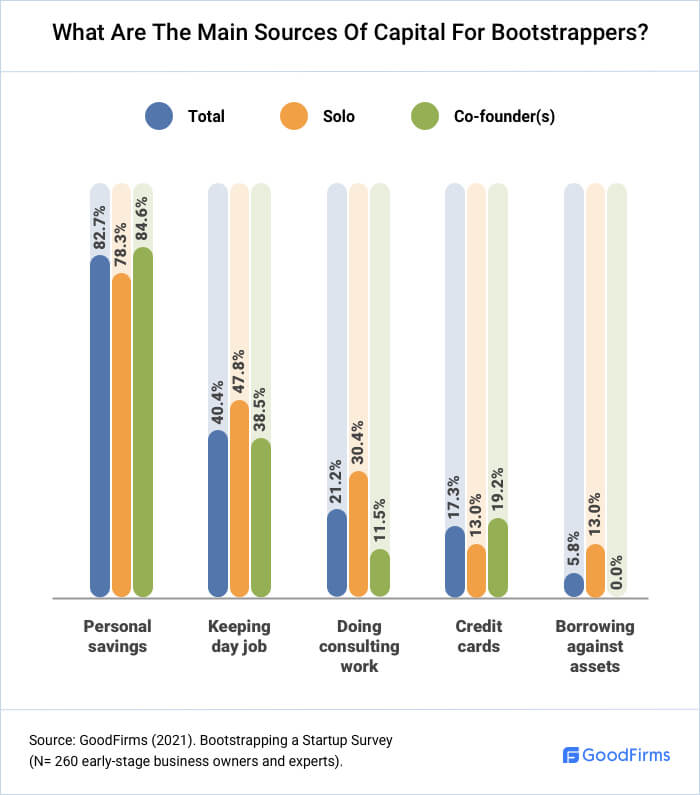

What are the Main Sources of Capital for Bootstrappers?

It's mainly in the beginner stages when the founder uses personal savings, loans from friends and family, credit cards, or continues with their jobs.

82.7% of the surveyed owners used savings to keep themselves afloat while finding a foothold. A 40.4% of the surveyed stayed in their jobs while working on the business in off-hours.

Savings - Using personal savings to build a business have benefits like greater ownership percentage and reduced interest on loans that one would need otherwise. However, you need to consider your net worth and contribute accordingly to your business.

Keeping Day Job - Keeping a job while starting a new venture allows you to have some guaranteed income and something to rely on in the worst-case scenario of business failure. However, you must check company policy first.

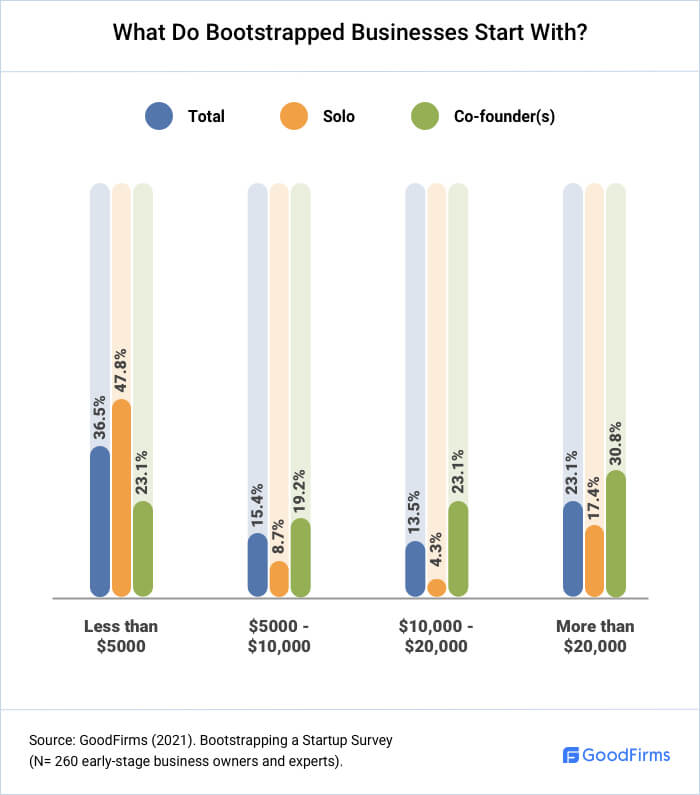

What Do Bootstrapped Businesses Start With?

There cannot be a specific dollar amount for individual industries as every business is unique, and costs depend upon various factors. You need to outline a detailed business plan, cash flow forecast, and determine capital expenditures.

However, a thoughtful adaptation of technology can make any business run on low finances. Goodfirms' survey reveals that 47.8% of the solo entrepreneurs bootstrapped a startup with less than $5000. In contrast, 30.8% of businesses with co-founders have more than $20,000 in the earlier stages.

Some industries require comparatively less capital to get started, and so work better with bootstrapping strategy. "eCommerce startups can often be bootstrapped. You can quickly and easily launch on platforms like Shopify from $29/month and you can plug-in to drop-ship suppliers so your capital outlay on inventory is zero, to begin with," says Michael Rosenbaum, CEO and Co-Founder of Spacer.

He adds, "Whether bootstrapping is right for you really depends on your business model & vision. Some models are not capital intensive, whilst others like SaaS and Marketplaces require large initial injections of capital to achieve scale, but then can be quite lucrative."

Advantages Of Bootstrapping A Business

Not every type of business, every model is ideal for bootstrapping. While comparing numerous types of funding, you need to weigh the pros and cons of bootstrapping to understand if a self-financed path is perfect for achieving your goals.

A company started in a more mature market with an already existing business model is a better candidate for bootstrapping and can have the following advantages.

1) Control Retention of Business

"Once you open up to outside investors, you accept that you're going to have to make concessions and ask permission. You won't be able to make moment-to-moment decisions about how your business is running, what your policies are, and who you hire. For some entrepreneurs, allowing other people to have a say in how their business runs isn't a big deal. For others, it's a nightmare. If you are someone passionate about executing your business strategy according to your vision and your vision alone, you're better off bootstrapping it," says Daivat Dholakia, Director of Operations at Force By Mojio.

2) Time-saving and Flexibility in Business Operations

Amit Prasad, CEO of QuickFMS, says, "The biggest advantage of bootstrapping in the initial stages is the time saved by entrepreneurs that would otherwise engage with investors.

- Suppose you get a group of private investors for a crowdfunding round. In that case, you have to engage them, keep them updated, handle their paperwork, and later address any concerns, give them regular updates about the business, etc. All these activities take time.

- If you get a professional fund or a more prominent investor, you need to do a lot of regulatory paperwork. Possibly give them a board seat and spend a lot of time on 'compliances' and implementing 'best practices,' which sometimes might not even be relevant at that stage of your organization.

Thereby eating up precious management time and resources, bootstrapping with your own money gives you a lot of flexibility on how to use your time and where to put focus on the main issue, growing your company profitably."

3) Operational Discipline

"Being flush with outside capital might often be a curse because you won't be as critical on how you spend your money. you may use it on unnecessary hires or software purchases that don't provide enough value to your company," says Neal Taparia, CEO of Solitaired.

He adds, "When you bootstrap a business, every dollar spent and made is yours, and it forces you to think about what is the most optimal way to use your time and capital. When initiative or hires don't work, it's your capital at risk, and you move faster to make the right decisions. Bootstrapping can give you a leg up on operational discipline that can allow you to be lean, nimble, and mean."

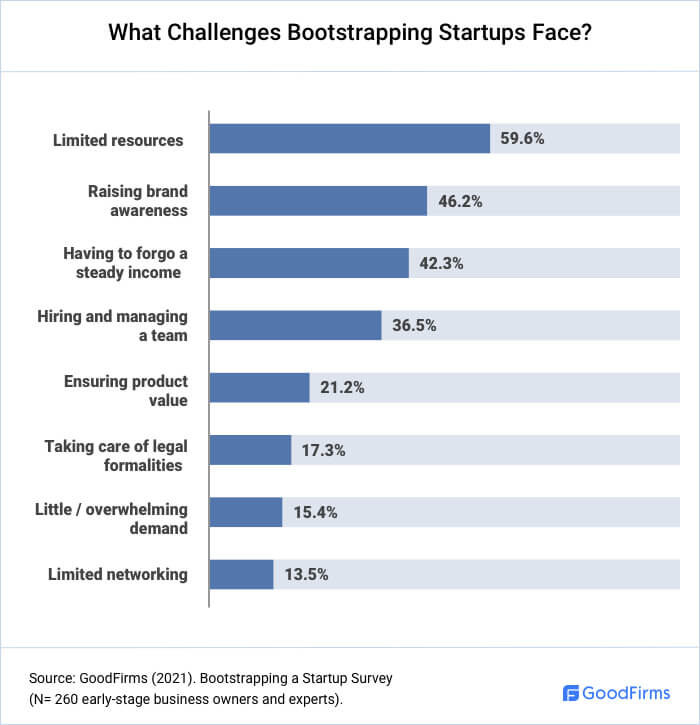

Challenges A Bootstrapping Startup Face

While bootstrapping startup ventures, entrepreneurs face quite a few challenges that demand critical decisions. As mentioned earlier, the fundamental concept of bootstrapping is utilizing one's own finances. Though it offers several benefits, it also limits founders' capacity to invest in infrastructure and human capital.

57.7% of the surveyed business owners consider limited resources as the biggest challenge while bootstrapping a startup.

David Jackson, CEO and Co-founder of FullStack Labs, talks about how lack of capital results in resource scarcity and how it challenges further progress. He says, "The companies built on new business models, new ideas and new markets, require a lot of upfront capital to get themselves off the ground. You have to have a huge sales force to go out and educate the market and educate buyers that this is something that they need. You need to have a huge R&D team building the product, to be able to sell it to the market."

Founders also cannot often make sense of brand awareness metrics and wonder whether they're making progress or not, as mentioned by 46.2% of them. They generally struggle with lack of content visibility, targeting the wrong audience, low engagement with digital advertising, inaccurate brand perception, and consequent poor rankings in search results. Founders can survive various challenges by adapting, iterating on, and improving their initial ideas based on feedback from actual or potential customers.

9 Tips For Bootstrapping A Startup

You can go for bootstrapping an idea you believe in wholeheartedly. Mentioned below are the tips you should keep in mind to ensure that the risk you take pays off.

1) Plan Your Budget

Estimating income and expenditure can be a bit intimidating for your bootstrapped startup because it will have little or no past performance to gauge against. However, planning a budget is essential to know when to adjust necessary variables and make predictions of cash shortfalls. Accounting services can assist you in allocating your limited resources, including machinery, labor, and cash, to accomplishing the business objectives.

"The most important part about bootstrapping is making sure you budget for every expense including office supplies, your phone bills, and even insurance. It's important to make an entire financial overview with projections, estimated costs for whatever you plan to sell and your overhead costs. Lastly, don't forget about taxes," says Oscar Hedaya, serial entrepreneur at SPACE.

Advising to put together a solid business plan, Oscar says, "Sometimes when you write everything out, you realize it is either the best idea or the dumbest idea. Once you have your budget, assume it will definitely be higher without you accounting for it; double or triple or quadruple - depending on what your business type is."

Daivat Dholakia says, "When bootstrapping a startup, it's critical to keep costs low at every opportunity.

- Use free/low-priced software for your communication, project management, accounting, and other operations.

- Start with a small staff that you can grow over time instead of a big team. Before you start rolling out a bunch of trendy perks to attract talent, check your accounts and see if it's financially feasible.

- Instead of renting that big fancy office in the hip neighborhood, be willing to settle for a smaller and less convenient space."

2) Register as a C Corporation

Budding entrepreneurs find it challenging to decide whether to register their startups as S Corp, C Corp, or LLC. A C-Corporation brings businesses greater growth potential and credibility. It differs from the other forms of business entity in ownership, taxation, and the ability to raise capital through stock.

"There is no better way of bootstrapping your startup than registering it as a C corporation. The major reason for this is that you won't be taxed for what your business earns and generates. The business and the owner are taxed separately when registered as a C corporation. If the business fails, you only lose your investment and are not liable to pay anything to the government agencies," says Janet Patterson, VP of Marketing Communications at Highway Title Loans.

3) Barter Your Services For Other Services

As self-funded startups struggle with limited resources, barter systems can help them use their working capital more productively, improve the overall operating efficiency, and improve their market share.

"You may be unaware, but you may possess information, skills, resources, and perhaps even connections that other entrepreneurs want, and vice versa. Determine what other entrepreneurs need and what you may be able to offer in return for what you lack on your end. Even simple actions such as acting as a connection or exchanging social media postings may help save expenses," says Ebony Chappell, Co-Founder & CMO of Formspal.

Dr. Amanda Holdsworth, CEO of Holdsworth Communications, also advises, "Figure out who you can swap services with. For example, when I first started doing enrollment marketing for my company, I swapped my PR services for another consultant's enrollment management services. So, I did some PR for her organization and she reviewed my clients' processes and email funnels at no cost."

4) Clear Daily and Weekly Goals

Businesses must look at the big picture and break down their goals into yearly, monthly, weekly, and daily goals. Accordingly, they should create an action plan for the week based on their key objectives. This will help them stay focused on the prioritized tasks, make them more productive, and improve work-life balance.

"When you're bootstrapping a startup you will likely be the content creator, marketer, webmaster, sales person, customer service representative, and business administrator all in one role. It requires a great deal of context-switching, which can be exhausting in a single day," says Jessica Maslin.

She adds, "The best way to get this done without burnout is to set clear daily and weekly goals. Of course, you may anticipate that Wednesday can be your creative day - and then customer service and sales calls come in, derailing your plan to create and schedule content. These are good problems to have; although you may not get the to-do list for that day done, it signifies that your business is moving forward. Don't let the unexpected derail your weekly goals."

5) Convert Your Customers into Your Evangelists

Every business benefits a lot from having customers who voluntarily become brand advocates. For instance, they can have a massive demand for the products and services, lower their customer acquisition costs (CAC), and multiply social capital.

"Make it easy for your new users and consumers to spread the word. People are fascinated by new businesses and innovations," says Teo Vanyo, CEO of Stealth Agents.

He gives suggestions, "Customers use social media to demonstrate to the rest of the world that they are cool, hip, and trendy.

- Provide opportunities for your early consumers to promote your startup to their social networks.

- Allow customers to access a discount voucher by sharing your website on social media or establish a branded hashtag and pick winners at random.

- You may even use a hashtag to showcase photographs of your consumers utilizing your product on your company's social media pages. You may build instant brand engagement by appealing to people's narcissism."

6) Scale Only When Your Business Needs It

Growing demand is certainly one factor that indicates the business's need for expansion. However, untimely scaling without sustainable demand can quickly derail the growth. Startups should gather, manage, and leverage data about current capabilities, future projections, and the infrastructure capacity for expansion to know the right time to scale.

"Knowing when to scale your bootstrapped startup is crucial to your success. Your product has to scale along with your business," says Saravana Kumar, CEO & Founder of Document360.

He adds, "Typically, when a product is launched, entrepreneurs begin looking for initial traction. As soon as they are able to crack that, they decide to scale their business. We must break this pattern to evade premature scaling. Products need to be put through consistent updates and extension cycles with users in mind until they reach the maturity stage. Only then, they can think about diversification and scaling."

7) Create a Long-term Strategy

Knowing where an entrepreneur wants to be in five or ten years helps them decide, strategize, and review the progress of short-term plans. Long-term goals could be anything from 'hire 100 new employees nationwide' to 'develop and launch five new products.' For long-term strategy, bootstrappers must include business growth, skills, debt, succession, and exit planning. Having insights from authentic resources helps improve business performance.

"Create a thoughtful, long term strategy and articulate it prior to any launch. Share it with at least one or two trusted sources that you value for critical feedback," says Tej Brahmbhatt, Senior Partner at Watchtower Capital.

He adds, "The best foundation for a new company is to have not only a Plan A (and backup plans) but also to have a roster of potential clients, partners, and advisors well before your proposed launch and fundraising. This creates a treasure trove of critical but elusive skills as well as the long-term benefit of building through slow, steady, and sustainable growth vs. seeking immediate, external funding."

8) Network, Network, Network

Networking is a perfect way to identify best business practices/industry benchmarks/trends, acquire new business leads, and stay on the cutting edge of technology. That is why entrepreneurs should use every professional and social opportunity to connect with new people.

"Business is all about who you know and it is important that you get your name out there. When I first jumped into Aloa full-time out of college, I was going to at least 4 networking events per week (pre-Covid). During the pandemic and now after, I do at least 3 purely networking calls per week," says David Pawlan, Co-Founder of Aloa.

He says, "Startups want to help each other, but you have to be willing to put yourself out there and learn from others. So many people have made every mistake out there, so the more you can network and learn from others, the more you can learn about what mistakes are common and how to avoid them. Don't trip on the first-timer's mistakes if you don't have to, learn from the experiences of others."

9) Use Social Media To Your Advantage

Market research on social media enables bootstrappers to have quantitative and qualitative data to better understand social, customer, or market trends. However, one must be clear whether the research is about the brand, products, consumer insights, online consumer behavior, customer service, or competitor insights.

Michelle Diaz, Head of Business and Analytics Team at OddsJam Inc, shares how they used Reddit to collect insights from their prospects before new product launching.

She says, "At OddsJam, we are building an innovative product for the US sports betting market. Since sports betting was still in just a few US states at the time, we looked for comments from Reddit users who said, "I wish there were ____." We reached out to these users to gather more information and ideas, simply letting them know we were entrepreneurs in the space, looking to build an innovative product that helped solve their problems.

Some Redditors were responsive; some were not. But, ultimately, once the product was done, we could reach back out to the responsive ones and get a tick up in customers on our first day in business, with $0 in marketing spend. This strategy has continued to work as we profitably bootstrap a business with almost no marketing spend. We reach out to users on Twitter and Reddit who bet on sports and have a mathematical background, and we ask them what they would like built."

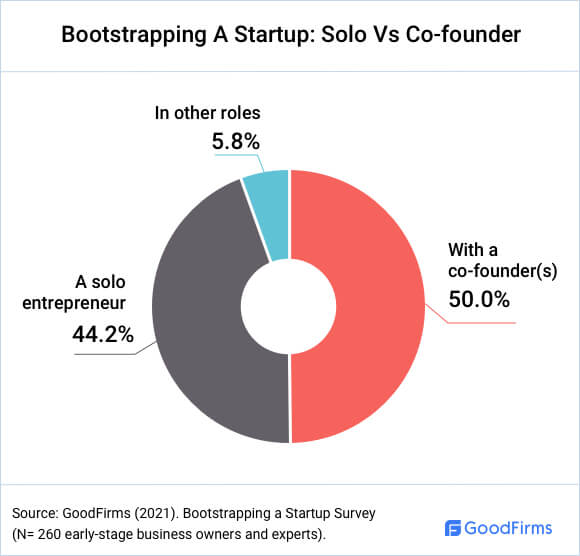

Bootstrapping Your Startup: Solo Vs Co-founder

Some entrepreneurs are lone wolves and want to thrive on a life of responsibility and daily challenges. While others believe in working on the tasks they are good at, leaving other jobs to someone better skilled.

50% of the surveyed startups prefer to have a co-founder(s), while 44.2% work as solo entrepreneurs.

Both the ways of going forward have their pros and cons. As a solopreneur -

- You can be entirely in charge of deciding how to run your business, where and when to work, what customers to go after, etc.

- You can also have complete control over financial matters such as bank accounts, company credit cards, and tax payments.

- Moreover, you don't have to worry about business partnerships going awry, which is often a possibility despite everyone's best intentions.

When running a business with a co-founder -

- You can come up with more innovative ideas through brainstorming and develop a solid backbone for your business. After all, when both the founders focus on the same end goal, a difference of opinion can be healthy and help you see the larger picture.

- You can enjoy a better work-life balance by dividing the responsibility based on the individual's complementing skill sets. When your co-founder shares the same vision as you, your business can reach new heights.

- When it comes to the later stage of looking for investors, often, a company with multiple founders is considered more stable and reliable.

"Being a solopreneur isn't a bad choice, but the right partnership divides the work and multiplies the success," says Paresh Sagar, CEO of aPurple.

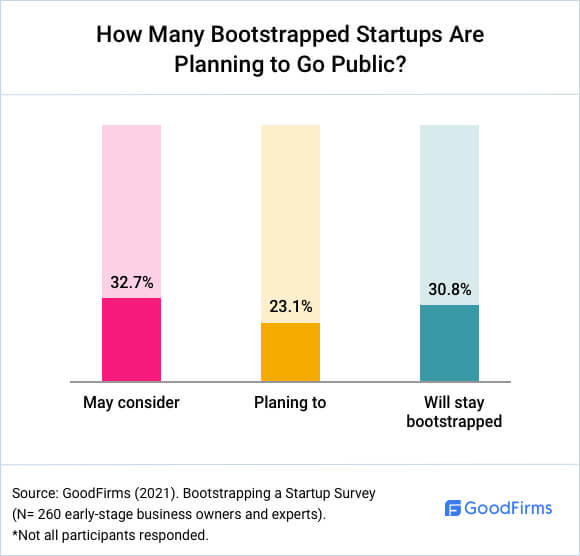

Should Bootstrapped Startups Go Public?

As stated earlier, bootstrapping is mainly adopted at the early stages of startups. Once entrepreneurs establish their basic business model, they focus on upgrading the equipment, hiring more employees, perhaps renting a bigger workplace, etc. So, many bootstrappers try to find venture capital or take out loans for expansion after reaching this stage.

32.7% of the surveyed bootstrapped startups might go public depending upon the circumstances, while 30.8% of the solo entrepreneurs do not want to relinquish their control.

There could be several reasons behind a company going for this challenging and time-consuming process of having an IPO. Such as:

- Spreading the ownership risk to a massive group of stakeholders

- Getting financing from somewhere else other than the banking system

- Reducing the total cost of capital

- Having more latitude while negotiating bank rates to reduce the interest on the debt

Going public is a significant milestone that requires thoughtful consideration. Here are some points to keep in mind:

- Your business has to be mature enough to reliably predict the next quarter and the year's expected earnings.

- There has to be plenty of growth potential in your business segment.

- It's better to be one of the top players in the industry.

- Have a strong management team in place.

Many giant listed companies, such as Facebook, Dell, Microsoft, GitHub, TechCrunch, Apple, have their humble roots in bootstrapping. Jamf, the standard in Apple enterprise management, had spent its early years in the bootstrapped wilderness. Finally, it started trading on the Nasdaq in July 2020.

Conclusion

Nowadays, more and more entrepreneurs prefer bootstrapping a startup even though it is nothing short of an adventure made of a series of mini-quests. Here, personal investments or operating revenues are at stake, so one must thoughtfully weigh all the pros and cons.

Self-funded startups face several challenges, such as having to forgo a steady income, operating with limited resources, raising brand awareness, hiring and managing a team, taking care of legal formalities, etc. However, founders can have much-coveted creative freedom and financial control without the need to justify everything to investors. After getting operational, many ventures with a strong traction scale begin looking for bank loans, lines of credit, or revenue-based funding. As a bootstrapped founder, follow the tactics shared by the experts here and 'pull your business up by bootstrapping strategically.'

About The Bootstrapping Survey

Goodfirms surveyed 260 early-stage business owners and experts to know the challenges bootstrapping ventures face and their solutions.

We sincerely thank our Research Partners, consisting of B2B (57.7%) and B2C (42.3%), for giving us insights into the strategies to bootstrap a startup successfully.

A mix of senior-level executives and business process managers took part in this survey. These included CEOs (26.9%), Founders (30.8%), Co-Founders (19.2%), Owners (5.8%), and other executives (17.3%).

These respondents belonged to various sizes of companies - 98.1% of Small Enterprises (1-249 employees) and 1.9% of Medium Enterprises (250 to 499).

* For any queries, drop an email to [email protected]

- Airfocus

- Akveo

- Allegiance Flag Supply

- Aloa

- Bella Terra Organic Spa

- Brenton Way

- BuyersGuide

- CocoSign

- Coffee Geek Lab

- Credit Donkey

- Denterica

- Diggity Marketing

- DoctorSpring

- Document360

- EDHEC Business School

- Eduard Klein

- Epilocal

- Firesticktricks

- Focus Insite

- Force By Mojio

- Formspal

- FullStack Labs

- Goldie Agency

- Highway Title Loans

- Holdsworth Communications

- Ivy Podcast Discovery

- Just SEO

- Kevin Miller

- Martial Arts on Rails

- Mashman Ventures

- Mavens & Moguls

- MCS Software Rental

- MELD

- Mieron VR

- Mind Bank Ai

- Mobibi, Inc.

- MyCorporation

- NAMYNOT Inc.

- OddsJam Inc

- Pilot Fish

- Poindexter

- QuickFMS

- RoverPass

- RRP Jewellers

- Sapochnick Lawfirm

- School Authority

- SO Productive

- Solitaired

- SPACE

- Spacer

- Stealth Agents

- Stone Wizards

- Test Prep Insight

- The Beard Struggle

- The Sky Floor, LLC

- Titoma

- Undergrads

- Watchtower Capital

- WeInvoice

- Zymmo