Key takeaways

- Sequencing determines survival: Neobanks built in a structured order, that is, regulation first, compliance next, followed by product development and growth, ensure stronger operational stability and consequently lower failure rates.

- Compliance is the primary risk: Weak KYC, AML, and fraud controls are the most common causes of early neobank shutdowns.

- BaaS accelerates market entry: Banking-as-a-serviceensures faster market entry and reduces development timelines compared to full-stack builds.

- Estimated development cost (Phases 1–4): $90k–$320k depending on scope, tech stack, and compliance setup.

- User demographics shape product architecture: Millennials and Gen Z comprise the majority of the neobank users, reinforcing the importance of mobile-first, automation-driven experiences.

Neobanks are flipping the script in the banking space. Unlike traditional or digital banks, they are not fully licensed banks. This means fintech startups can launch a neobank by leveraging what Goodfirms refers to as Neobank Vendor Recipe - a framework that outlines how digital banks progress from regulatory foundations to scalable growth.

The idea behind launching this recipe is to address the growing number of neobank failures. Goodfirms' close-knit group of researchers found that several prominent neobanks that failed between 2023 and 2026 had effectively "put the cart before the horse," prioritizing rapid growth over establishing regulatory and compliance foundations.

In other words, the nuts and bolts of a neobank (read: the tech stack), if not structured sequentially results in operational instability when faced with fraud and regulatory risk.

A notable example is Azlo, a U.S.-based neobank backed by BBVA, which was shut down in 2020 due to regulatory and operational restructuring. The case illustrates a key reality of the fintech ecosystem: poor banking orchestration is often punished by regulators rather than competitors.

Building a neobank typically costs $90,000–$3,200,000across four phases: regulatory setup, compliance systems, technology development, and operational launch. This upfront investment ensures proper sequencing and reduces legal, operational, and financial risks. Our industry research further indicates that over 70% of fintech startups fail due to compliance and regulatory gaps, and regulators have repeatedly imposed fines or operational restrictions when financial controls remain immature.

Build Your Neobank the Right Way - Start Your Neobank Journey by Exploring Goodfirms Neobank Vendor Recipe.

Research Methodology

This research was conducted by Goodfirms Researchers using a mixed-method analytical approach.

The study examines the patterns of neobank development observed between 2023 and 2026.

Primary focus areas include regulatory strategy, BIN sponsorship, BaaS adoption, compliance systems, and product architecture.

Geographic coverage spans key fintech markets across North America, Europe, Asia-Pacific, and Latin America.

Data sources include: Industry and market research reports, regulatory and public financial records, Neobank product launch and closure data, and fintech infrastructure and vendor documentation.

The framework is based on an analysis of neobank launch structures, fintech infrastructure providers, and banking partnerships across global markets.

Neobank initiatives were evaluated using a four-phase sequencing model:

Foundation → Compliance → Product → Growth. Findings were validated through cross-source comparison and structural dependency analysis.

How Goodfirms Formalizes Neobank Development: The Four-Phase Model

To address the risks associated with poor banking orchestration, the Goodfirms think-tank developed the Goodfirms 4-Phase Neobank Development Model, a framework that sequences regulation, compliance, product development, and growth to help fintech startups launch neobanks more safely and sustainably.

.jpg)

This framework provides founders and investors with a fail-safe development sequence in sync with regulatory and operational requirements. More on this in a minute.

Market Drivers Behind Neobank Growth

Neobank adoption is fueled by changes in consumer and enterprise behavior worldwide:

- Smartphone-centered financial activity

- Reduced tolerance for physical branch processes

- Growth of cross-border and remote workforces

- Demand for fee transparency

- API-based service integration

Neobanks succeed through faster onboarding, real-time visibility into financial transactions, and simplified transaction flows. Their growth reflects changing expectations in the banking space, as digital services are increasingly valued over physical institutions.

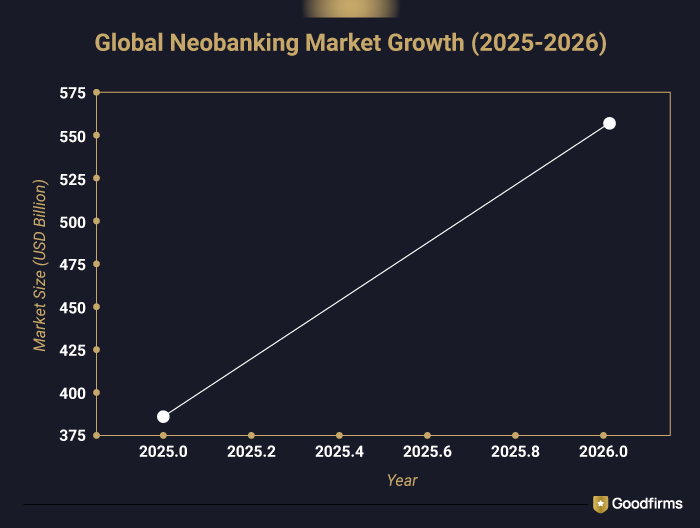

Global Neobank Market Opportunity

The global neobanking market is projected to reach $552.0 billion in 2026, up from $382.8 billion in 2025, indicating speedy adoption of mobile-first banking services among global users.

Additional indicators:

-

United States projected users: 34.7 million by 2026

-

AI-driven fraud detection accuracy: up to 96%, with false positives reduced by 50%

-

Growth driven by youth demographics, underbanked populations, and digital-native enterprises

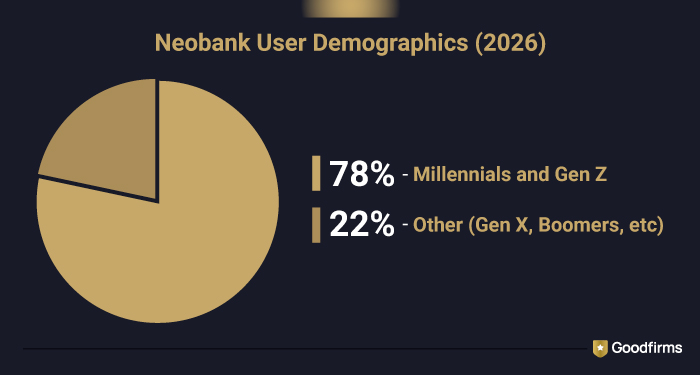

Neobank User Demographics

Millennials and Gen Z account for 78% of the active neobank user base.

Remaining users include Gen X and Boomers, who adopt digital banking for limited use cases, such as international transfers and portfolio tracking.

Strategic implication: Product design, feature prioritization, and onboarding experiences must align with user expectations for speed, automation, and digital integration.

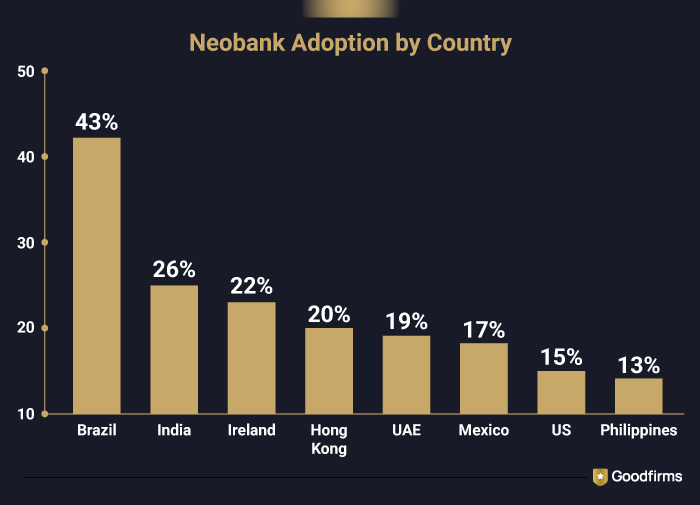

Neobank Adoption by Country

Currently, Brazil is leading the neobank market, while India and Ireland are catching up. thanks to high mobile-driven adoption. Emerging markets are demonstrating strong growth, driven by financial inclusion and the expansion of mobile banking.

While adoption continues to quicken across global markets, launching a successful neobank, as mentioned, requires more than market demand. It requires careful sequencing that aligns regulatory, technological, and operational components.

From Market Opportunity to Execution: How Neobanks Should Be Built

Launching a neobank requires careful orchestration of regulatory partnerships, compliance systems, technology infrastructure, and operational capabilities. Unlike traditional banks, neobanks must assemble these components through external partners while maintaining regulatory integrity.

To address these structural challenges, our research team developed the 4-Phase Neobank Development Model, which sequences the key stages for building and scaling a compliant digital bank.

The model breaks neobank development into four operational phases, from regulatory foundations to growth operations.

Phase |

Core Focus |

What Happens in This Phase |

|---|---|---|

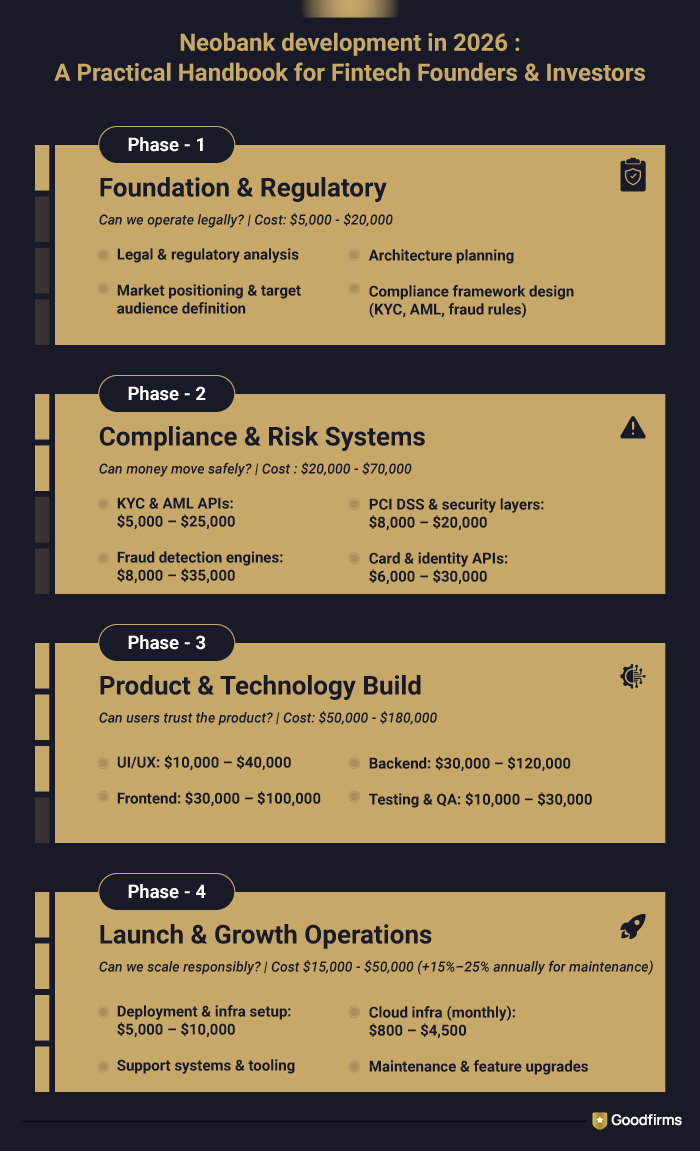

Phase 1 — Foundation & Regulatory |

Legal & Banking Legitimacy |

Sponsor bank setup, licensing structure, BIN sponsorship, governance, and capital planning |

Phase 2 — Compliance & Risk Systems |

Risk control and regulatory readiness |

KYC/AML frameworks, fraud detection, transaction monitoring, security, and reporting systems |

Phase 3 — Product & Technology Build |

Platform development |

Core banking integration, mobile app, payment rails, APIs, and infrastructure |

Phase 4 — Launch & Growth Operations |

Controlled scaling |

Customer onboarding, marketing, support operations, and continuous compliance tuning |

“In fintech, demand creates opportunity — but sequencing determines survival.”

Phase 1: Pre-Launch — Foundation & Regulatory (3–6 Months)

Strategic Implication: Phase 1 establishes the structural and legal base of the neobank. This phase should precede product development, with a focus on regulatory positioning and organizational structure.

To help you lay strong structural foundations, Goodfirms has identified the first vendor categories that you need to collaborate with:

- Licensing & Regulatory Advisory

- BIN Sponsor Partners

- BaaS Platform Providers

However, before you choose your vendors or technology, decide who your neobank is for.

1.1 Define Your Target Audience & Positioning

A neobank can realistically serve only one primary audience segment due to:

- Limited initial product scope

- Regulatory and structural constraints

In short, a NEW neobank cannot effectively serve multiple demographics right out of the gate.

This means you need to choose one clear audience segment first:

- Freelancers and gig workers

- Small businesses and startups

- Students and Gen Z

- Migrant workers and expats

- Creators and digital nomad

- Underbanked consumers

Think about how you’ll position your Neobank in the market and in users’ minds.

Positioning Formula:

We are the neobank for [user type] who need [main benefit] to address [main frustration].

Operational Significance: The target customer segment directly determines the appropriate licensing pathway, the sponsor bank selection, the core MVP feature set, and the pricing structure.

Evaluation Focus:

- Define your primary user segment

- Identify 3–5 core financial pain points of your target audience

- Write your one-sentence positioning

- Validate demand through interviews or surveys

1.2 Regulatory Strategy & Pathway

Your regulatory strategy defines how your neobank will legally operate.

You need to decide whether to:

- Pursue a full banking license

- Partner with a sponsor bank

- Use a BaaS platform with built-in compliance

Work with regulatory compliance consulting firms to document requirements and risks before building.

Operational Significance: The selected licensing pathway determines allowable product offerings, customers’ fund custody architecture, and jurisdictional market access

Caveat: Starting without a license plan exposes you to regulatory risk and potential disruptions.

Evaluation Focus:

- Map target jurisdictions (US, EU, APAC)

- Compare license vs sponsor bank vs BaaS models

- Engage regulatory advisory firms

- Document compliance obligations

Goodfirms insight: Neobanks that plan for regulation from day one launch faster and face fewer legal roadblocks than those that consider compliance only later in development.

1.3 BIN Sponsor Partners Selection

BIN sponsor banks provide the regulated banking license and infrastructure needed to issue accounts and cards.

BIN sponsorship structures enable:

- Account creation

- Card issuance sponsorship

- Settlement and custody services

- Regulatory coverage

Operational Significance: Your sponsor bank controls: vendor approvals, compliance standards, and product limits

Evaluation Focus:

-

Review sponsor bank compliance policies

-

Confirm approved KYC/AML vendor lists

-

Understand revenue-share models

-

Negotiate integration support and SLAs

1.4 BaaS Platform Decision

A Banking-as-a-Service (BaaS) provider can save you from building core banking features from scratch. In other words, it will offer a suite of APIs that enable effortless integration of banking services into a fintech’s platform.

But you must decide between:

- Integrated platform (all core services bundled)

- Best-of-breed (pick specialists for each function)

BaaS platforms bundle:

- Core ledger

- Compliance layers

- Payment and card APIs

Operational Significance: Reduces engineering complexity and launch time.

Evaluation Focus:

- List required backend functions

- Compare integrated vs modular stacks

- Evaluate API maturity and uptime

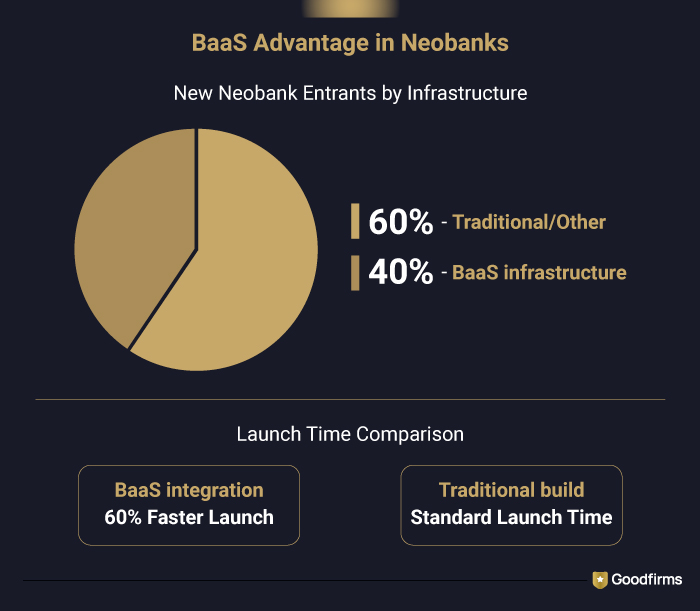

The BaaS Advantage

By utilizing Banking-as-a-Service (BaaS) infrastructure, neobanks effectively trade high capital expenditure and long development cycles for speed and agility.

1.5 Compliance Framework (strategy only)

In Phase 1, you just design the compliance framework, not deploy.

In this phase, you need to define:

- KYC workflows

- AML thresholds

- Fraud risk rules

- Reporting structure

Operational Significance:

Determines the ability to scale safely and avoid regulatory penalties

Evaluation Focus:

- Map KYC/AML flows

- Define escalation rules

- Assign compliance ownership

- Document policies

Phase 1 Outcome

✔ Target audience defined

✔ Regulatory model chosen

✔ Sponsor bank or BaaS path set

✔ Compliance framework documented

Phase 1 is the bedrock of a neobank. If this is not strongly built, everything built above it becomes fragile.

Estimated Cost for Phase 1: $5,000 – $20,000

Why does this phase cost what it does?

- Legal & regulatory analysis

- Market positioning & target audience definition

- Architecture planning

- Compliance framework design (KYC, AML, fraud rules)

Key Insights:

Goodfirms Research Observation: Avoid adopting a full licensing model when you launch because it’s: extremely expensive, takes 2–5 years, requires heavy capital, has high regulatory risk, is rarely granted to early-stage startups.

Phase 2 — Compliance & Risk Systems (4–6 Months)

Strategic Implication: This phase ensures secure money movement, fraud prevention, and regulatory compliance across all operational channels.

2.1 Card Issuing Platforms

Card-issuing platforms enable neobanks to create and manage virtual and physical payment cards for their users.

These systems enable:

- Virtual cards

- Physical cards

- BIN-level card programs

Operational Significance: Ensures users can transact seamlessly and reduces operational failures related to card issuance.

Evaluation Focus:

- Launch virtual and physical card programs

- Validate BIN-level integration

- Monitor initial transaction success rates

2.2 Card Processing Partners

Card processors ensure payments are authorized, cleared, and settled on time.

Processors handle:

- Transaction authorization

- Clearing and settlement

- Refunds and chargebacks

Operational Significance:

Payment reliability is critical; failures directly erode trust and brand credibility

Evaluation Focus:

- Test transaction processing across payment networks

- Verify refund and chargeback handling

- Monitor processing speed and uptime

2.3 KYC / KYB Platforms

KYC and KYB platforms check the identity of people and companies before they open accounts.

Identity verification systems:

- Validate users

- Verify businesses

- Detect document fraud

Operational Significance: KYC/KYB is the first line of defense against fraud, financial crime, and regulatory penalties.

Evaluation Focus:

- Implement identity verification workflows

- Monitor verification success and failure rates

- Ensure compliance with jurisdiction-specific KYC/KYB rules

2.4 AML Screening & Transaction Monitoring

AML software systems continuously watch money movements to detect unusual transactions linked to crime.

AML systems:

- Monitor transactions

- Flag suspicious behavior

- Generate regulatory reports

Operational Significance:

Prevents criminal misuse of the platform and avoids regulatory sanctions.

Evaluation Focus:

- Define AML thresholds and monitoring rules

- Test alert generation for suspicious transactions

- Validate reporting outputs for regulators

2.5 Fraud & Risk Management

Fraud and risk detection tools use behavioral analysis and transaction patterns to prevent unauthorized activity.

Fraud tools detect:

- Account takeovers

- Card fraud

- Behavioral anomalies

Operational Significance:

Protects margins, user trust, and brand reputation.

Evaluation Focus:

- Configure behavioral risk models

- Run simulations for fraud detection efficacy

- Monitor incident response and resolution timelines

Phase 2 Outcome

- Cards and payments live

- Identity and AML systems active

- Fraud prevention running

Estimated Cost for Phase 2: $20,000 – $70,000

Why does this phase cost what it does?

- KYC & AML APIs: $5,000 – $25,000

- Fraud detection engines: $8,000 – $35,000

- PCI DSS & security layers: $8,000 – $20,000

- Card & identity APIs: $6,000 – $30,000

Phase 3:Product & Tech Build (3–4 Months)

Strategic Implication: This phase delivers the customer-facing neobank app and the technology infrastructure that supports secure, scalable daily banking operations.

3.1 Neobank App Development

Neobank app development companies focus on building the mobile and web interfaces that customers use to access banking services.

Neo bank app development includes:

- Digital onboarding

- Account dashboard

- Payments and transfers

- Transaction history

- Customer support flows

Operational Significance:

The app serves as the primary touchpoint with users.

Evaluation Focus:

- Test onboarding flow completion rates

- Monitor transaction success and error rates

- Validate customer support integration

- Collect usability feedback from pilot users

3.2 Backend/ API Integrations

Backend systems connect your app with core banking services, payment networks, and third-party platforms.

Backend and API developers handle:

- Core banking integrations

- Payment system connections

- Partner APIs

- Data synchronization

Operational Significance:

Reliable API integrations are essential for uninterrupted banking operations and regulatory compliance.

Evaluation Focus:

- Perform end-to-end API testing across all services

- Monitor data consistency and synchronization

- Validate system redundancy and failover processes

3.3 Fintech UI/UX Design

Fintech web design agencies shape how users navigate, understand, and trust your digital banking experience.

Design work includes:

- User journey mapping

- Interface layouts

- Accessibility optimization

- Conversion-focused flows

Operational Significance:

Well-designed interfaces reduce churn, increase engagement, and strengthen user trust.

Evaluation Focus:

- Conduct usability testing and A/B experiments

- Analyze navigation efficiency and task completion rates

- Validate accessibility compliance and conversion metrics

3.4 Fintech Cybersecurity

Fintech cybersecurity companies protect user data, financial assets, and internal infrastructure from attacks.

Core security layers include:

- Data encryption

- Secure authentication

- Penetration testing

- Vulnerability monitoring

Operational Significance: Security failures compromise user trust, regulatory compliance, and the bank’s credibility.

Evaluation Focus:

- Perform penetration testing and vulnerability scans

- Validate encryption and authentication protocols

- Monitor incident response times and resolution effectiveness

Phase 3 Outcome

✔ Working neobank app

✔ Secure infrastructure

✔ Integrated systems

Estimated Cost for Phase 3: $50,000 – $180,000

Why does this phase cost what it does?

- UI/UX: $10,000 – $40,000

- Frontend: $30,000 – $100,000

- Backend: $30,000 – $120,000

- Testing & QA: $10,000 – $30,000

Phase 4: Launch & Growth — Scaling Operations

Strategic Implication: With the product live and compliance systems operational, Phase 4 focuses on attracting users, supporting them effectively, and establishing scalable operational processes.

At this stage, your focus should shift from building technology to delivering value and growing responsibly.

Goodfirms groups this phase under two key service areas:

4.1 Digital Marketing & Advertising

Fitech digital marketing and advertising agencies drive brand awareness and user acquisition for your neobank.

Key marketing activities include:

- Search engine marketing (SEO and PPC)

- App store optimization (ASO)

- Paid social and display ads

- Content marketing campaigns

Operational Significance:

Visibility and targeted messaging directly influence adoption rates and initial traction.

Evaluation Focus:

- Monitor cost-per-acquisition (CPA) and conversion rates

- Track engagement metrics across channels (click-through, downloads, installs)

- Analyze campaign ROI and optimize spend allocation

- Test messaging and creatives for user resonance

4.2 Customer Support

Fintech customer support ensures that user queries, disputes, and service issues are addressed efficiently across multiple channels.

Support operations include:

- In-app chat support

- Email and ticketing systems

- Call center assistance

- Automated chatbots

Operational Significance:

High-quality support enhances user retention, brand trust, and long-term loyalty.

Evaluation Focus:

- Measure response time and first-contact resolution rates

- Track ticket volume trends and escalation patterns

- Assess user satisfaction via surveys and NPS

- Evaluate chatbot performance and accuracy

Phase 4 Outcome

By the end of Phase 4, you should have:

- A live neobank with active users

- A defined go-to-market strategy

- Scalable marketing channels

- A trained customer support operation

- Operational dashboards

- Measurable user growth and retention

At this stage, your neobank is no longer just a product. It is a running financial business with: Real customers, real transactions, and real operational risk

Estimated Cost for Phase 4: $15,000 – $50,000 (first year)

+ 15%–25% annually for maintenance

Why does this phase cost what it does?

- Deployment & infra setup: $5,000 – $10,000

- Cloud infra (monthly): $800 – $4,500

- Support systems & tooling

- Maintenance & feature upgrades

Neobank App Development Cost Phase-Wise

| Phase | Focus | Cost Range | Development Timeframe |

|---|---|---|---|

| Phase 1 | Strategy & regulation | $5,000 – $20,000 | 3–6 months |

| Phase 2 | Compliance & risk systems | $20,000 – $70,000 | 4–6 months |

| Phase 3 | Product & tech build | $50,000 – $180,000 | 3–4 months |

| Phase 4 | Launch & operations | $15,000 – $50,000 + 15–25% yearly | Ongoing (post-launch) |

Key Observations:

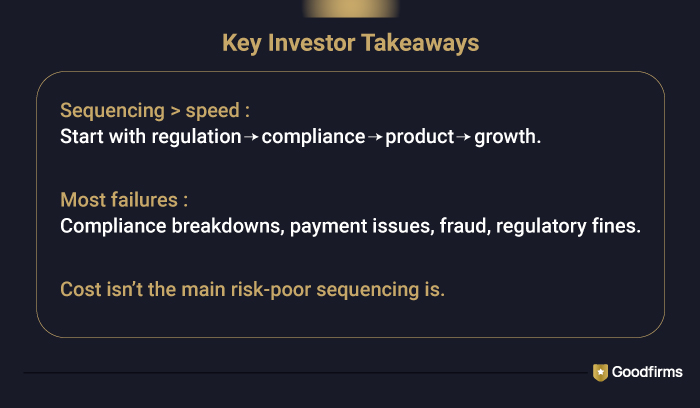

Key Insight: Sequencing is more critical than the cost of neobank development; poor sequencing drives legal, operational, and trust failures.

Common Risks & Failure Points

Many neobanks fail not because of weak ideas, but because of hidden operational weaknesses.

Strategic Risks

- Choosing the wrong target audience

- No clear path to profitability

- Expanding into too many products too fast

Regulatory & Compliance Risks

- Weak KYC and AML controls

- Incomplete reporting

- Ignoring sponsor bank rules

Technology Risks

- Rigid, monolithic systems

- Poor API integrations

- No disaster recovery

Vendor Risks

- Working with unvetted partners

- Over-dependence on one provider

- Weak SLAs

Why this matters to investors:

Most neobank shutdowns are caused by:

- Compliance failure

- Payment breakdowns

- Fraud losses

- Regulatory pressure

Final Insight from Goodfirms

The neobanks that win in 2026 will not be the fastest to launch, but the ones built in layers.

They invest first in regulation, then in technology, and finally in growth systems.

Regulation first. Compliance second. Technology third. Scale last.

In banking, cost is not the primary risk. Poor sequencing is.